Health Insurance Death Spiral: How to Stop Group Health Insurance Premium Increases

- March 31, 2018

- Posted by: Gus Altuzarra

- Category: Healthcare Cost Increases

Health insurance premiums are a derivative of health care costs

In its purest form, insurance is a just a derivative of cost. You take the total cost of all expected claims of a group of people or companies, you divide it by the number of payers, add on the administration expense of the coverage (normally 15-30%) and you pop out a premium.

Insurance has been used as a tool since the mid 1700’s in the United States to transfer risk. Since then the industry has grown considerably to $1.274 trillion in gross premiums in 2013. One thing has not changed – the premiums you pay are a derivative of the cost.

I’d like to argue that insurance itself is not the problem when it comes to health care in the United States. Yet everyone is talking about the issues with health insurance and “high premiums”. What really is the root problem here? And how can we stop group health insurance premium increases?

Health insurance companies are doing a very poor job of managing the cost of health care

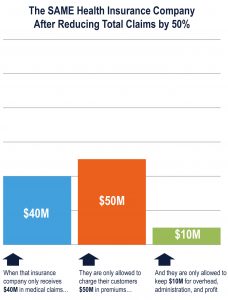

You might think intuitively that a health insurance company would like to reduce claims because the more they save in claims the more money they make, right? It’s actually the complete opposite. Health insurance companies have a financial incentive to keep your premiums high. The Affordable Care Act established a “Medical Loss Ratio” which requires each insurer to spend 80% of it’s premium dollars on claims. This makes sense in theory but for a public company with a fiduciary responsibility of increasing profits and share holder value, there is a conflict of interest. The only way a health insurance company can increase profits is by increasing premiums.

Most large PPO networks boast about their large number of professionals and how they can cut the cost of a typical doctors visit or surgery. Pull back the curtain and you’ll see these discounts are just an accounting trick. To allow PPOs to advertise big discounts, providers simply inflate their billed charges. If a provider raises the cost of a medical procedure, insurers can charge higher premiums, while also boosting the value of their shares.

In this way, the MLR rule encourages insurers to ignore providers’ artificial price hikes. Insurers can continue to attract customers with the promise of steep discounts through their PPO plans and providers can continue to drive up their prices. By gauging their customers, both insurers and providers make more money. And since insurance costs are just a derivative of health-care costs, the result has been a steady rise in insurance costs for millions of working families since the enactment of the ACA in 2010, thus creating the “death spiral”.

Solution for Businesses

If you manage a business health plan with at least 25 enrolled your best bet is to self-insure or use a level funded program. Here’s why:

- Claims transparency. You know how much you’re paying and how much you’re spending every year. With claims data you can customize wellness plans and plan for the future.

- Dividend eligible. You have a claims fund and any premiums that are not used for claims are returned to you at the end of the year – not the insurance company.

- Once you are in the right program it makes sense for you to start implementing cost control strategies. Well performing groups should be spending $6-$8K/yr per employee (including dependents) on health care expenses. A dollar saved is a dollar earned. These strategies include employee steerage to quality, affordable care, fiduciary PBMs, $0 Copay telemedicine, medical bill review, health fairs, and performance-based compensation. See my next article on health care cost control strategies for a more in-depth explanation of these strategies.

In short, it doesn’t make sense to rely on these large insurance companies to help keep health care costs down, they would lose too much money! Only those companies who take the time to educate themselves and take the reins on their own programs will be able to free themselves from the health insurance death spiral.

great information Gus, it makes a lot of sense.